Insurance is a document business. Policies, broker packs, adjuster notes, lab reports, medical records and photos—most of it is unstructured text or images. An effective insurance document management system turns those files into searchable, auditable data that fuels ai underwriting, claims decisions and service workflows. Below I unpack why legacy stacks fail, how modern systems work, use cases, benefits, implementation steps, real examples, and what Alltius brings to the table.

Introduction: the document problem, stated plainly

Carriers and brokers drown in documents. Underwriters spend hours reading broker submissions; claims teams sift through PDFs and scans; compliance teams hunt for signed forms. This friction delays decisions, creates rework and increases cost. Modern solutions that combine OCR, nlp insurance models and automated pipelines let organizations extract facts, preserve context, and route the right documents to the right people or systems.

Why traditional insurance document management systems fall short (deep dive)

Legacy systems typically store documents but don’t understand them. Key shortcomings:

Shallow extraction:

Basic OCR converts images to text but misses meaning—policy clauses, exclusions, ICD codes, or clause deltas.

Siloed storage:

Files live in claims, underwriting, or legal repositories with inconsistent metadata. That breaks search and reuse.

Manual validation:

Humans still validate numbers, reconcile dates, and check signatures—tasks that create bottlenecks.

Poor integration:

Legacy stacks don’t stream structured outputs into underwriting or claims engines, so downstream automation can’t run reliably.

Governance gaps:

Auditors need traceability—who corrected what field and why. Old systems often lack that provenance.

These gaps make the question “how will AI affect the insurance industry” less theoretical and more operational: the industry can only scale better document workflows if it solves these core technical and governance issues.

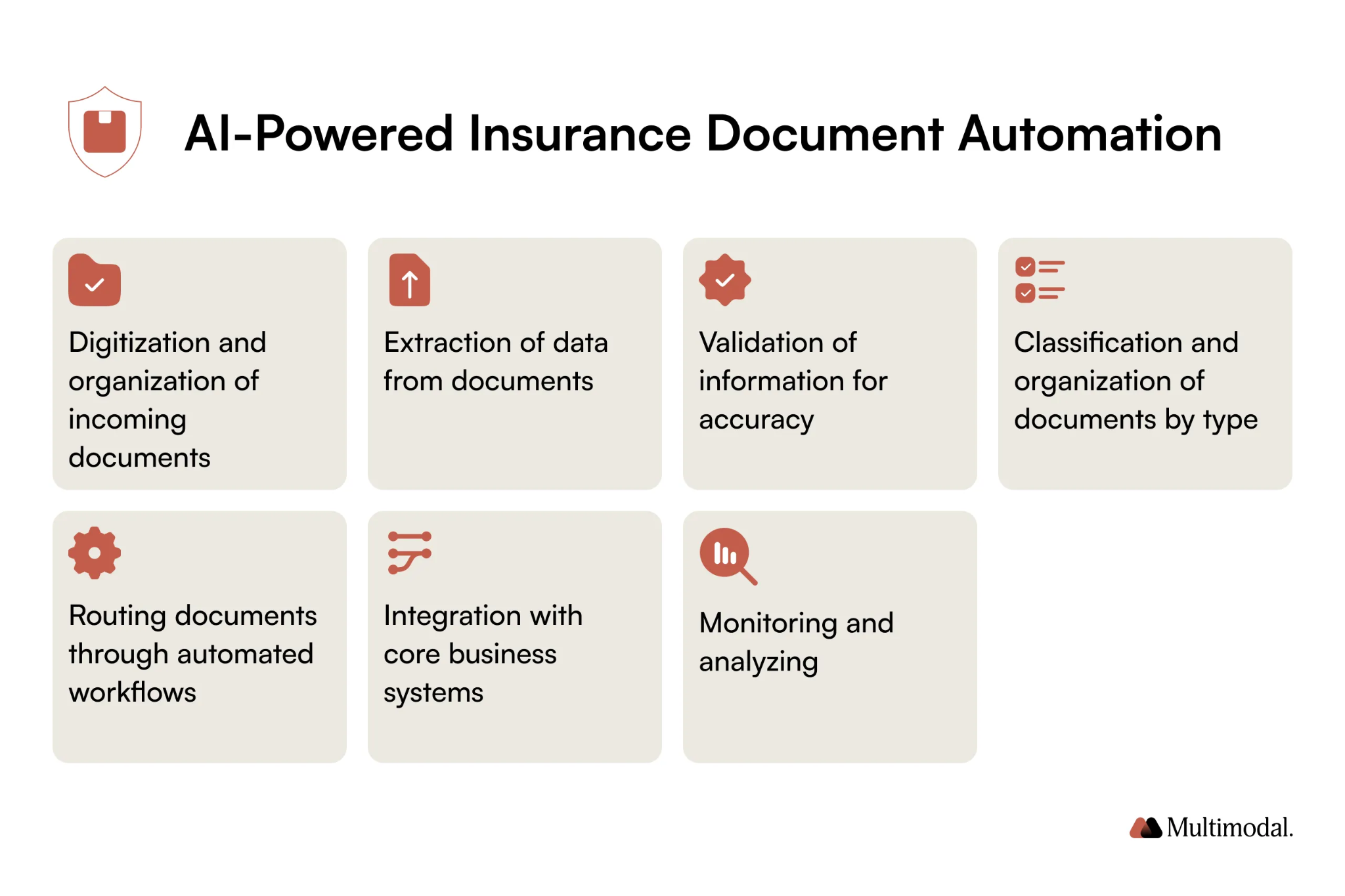

How AI Actually Handles Unstructured Insurance Documents: Step by Step

Step 1: Ingestion & Normalization

Collects documents from multiple sources like email, broker portals, SFTP, or scanners.

Removes duplicates, applies standardization, and prepares documents for downstream analysis.

Step 2: Optical Character Recognition (OCR)

Converts scanned images and PDFs into machine-readable text.

Advanced OCR now manages noisy scans, low-resolution documents, and even handwriting.

Step 3: NLP Insurance Models

Extracts critical information with specialized models:

Named-entity extraction: Identifies policy numbers, ICD/CPT codes, coverage limits, etc.

Relation extraction: Maps connections, e.g., which loss event attaches to which policy.

Classification: Sorts documents into categories such as claims, endorsements, or medical reports.

Step 4: Contextual Parsing

Goes beyond extraction to analyze context.

Performs clause-level parsing and detects redlines or variations across endorsements and policies.

Step 5: Confidence Scoring & Human-in-the-Loop

Each field is assigned a confidence score.

Low-confidence outputs are flagged for human review.

Human corrections are fed back into the models, improving accuracy over time.

Step 6: Delivery & Integration

Transforms extracted insights into structured data.

Pushes this data into underwriting platforms, claims systems, or data lakes.

Maintains a full audit trail with confidence scores for compliance and transparency.

👉 This stepwise pipeline ensures AI doesn’t just extract numbers, but provides reasons, evidence, and contextual clarity—crucial for underwriting, claims management, and regulatory compliance.

What it does: Extract claimant details, incident descriptions, provider bills, and EOBs; automatically tie documents to the claim record.

Why it matters: Faster FNOL routing, fewer missing attachments, and earlier identification of potential fraud or coverage gaps.

Underwriting submissions

What it does: Parse broker packs, past loss runs, inspection reports, and medical histories; surface exposures, exclusions and key dates.

Why it matters: Underwriters get structured risk summaries rather than raw PDFs—reducing time to quote and improving risk selection.

Policy servicing and endorsements

What it does: Automatically compare endorsement wording against base policy and flag changed clauses or retro dates.

Why it matters: Fewer post-issuance issues and fewer manual checks.

Regulatory compliance & audit readiness

What it does: Continuously scan policy files for required disclosures, KYC documents, and retention rules.

Why it matters: Fewer fines, faster audits, and automated evidence packs.

Medical necessity and utilization review (health)

What it does: Map clinical notes to coverage rules and past authorizations; pre-populate reviewer summaries.

Why it matters: Speedier decisions, fewer appeals, better patient outcomes.

Tangible Benefits of an Insurance Document Management System with AI

One of the biggest challenges insurers face is separating the hype of AI from the hard numbers that executives actually need: cycle time, leakage, cost per file, and NPS. Below, we break down the concrete benefits and how they translate into business KPIs.

1. Speed: From Weeks to Hours

Traditional underwriting and claims processing rely on human reviewers to manually sift through policy documents, loss runs, medical records, and compliance forms. This often stretches cycle times from several days to weeks.

AI-enabled document systems read, parse, and classify thousands of pages in minutes.

Workflows that once queued in backlogs (such as FNOL intake or specialty line underwriting) can now move same-day.

Business KPI impact: Faster quote delivery and claims resolution increase placement rates and customer satisfaction.

👉 Why it matters: In commercial underwriting, shaving days off response time can mean winning or losing a renewal against a faster competitor.

2. Accuracy: Reducing Human Error

Manual data entry is inherently error-prone: missed clauses, mis-typed policy numbers, or overlooked endorsements often lead to costly leakage.

AI document intelligence flags anomalies, checks clause completeness, and ensures mandatory disclosures are present.

It reduces rework for underwriting assistants and minimizes downstream disputes.

Business KPI impact: Lower leakage and fewer disputed claims improve combined ratios directly.

👉 Why it matters: Missing a single exclusion clause in a specialty liability policy can expose the carrier to multimillion-dollar exposure — an avoidable risk when AI validates every word.

3. Cost: Shifting Human Effort to Value-Added Work

Insurers spend significant operating budgets on back-office processing. According to McKinsey, administrative costs represent 15–20% of premium in many carriers.

Automating data extraction and classification frees skilled underwriters to focus on exceptions, judgment calls, and risk strategy instead of rote typing.

Over time, staff can be redeployed toward growth areas like product development or customer engagement.

Business KPI impact: Reduced “cost per file” and measurable improvements in operational expense ratios.

👉 Why it matters: Cutting a few dollars per file scales into millions in savings across high-volume personal lines books.

Customers don’t see the back-office effort — they see the result: how fast they get a quote or a claim settled.

AI shortens response times dramatically, which directly boosts customer Net Promoter Score (NPS).

More accurate processing also means fewer frustrating back-and-forths.

Business KPI impact: Higher retention, improved cross-sell opportunities, and stronger broker satisfaction.

👉 Why it matters: In a competitive insurance market, a broker who consistently gets a same-day quote from one carrier will prioritize that carrier’s products.

5. Governance: Auditability and Compliance at Scale

Regulators expect strict adherence to documentation standards — and audits can be disruptive if compliance gaps exist.

AI-driven document management automatically logs every decision, providing a full audit trail.

Continuous compliance checks ensure no renewal slips through missing mandatory clauses or disclosures.

Business KPI impact: Reduced regulatory fines, fewer escalations, and better risk governance.

👉 Why it matters: A regional insurer flagged by regulators for documentation lapses risks reputational damage and higher capital requirements — issues that automation prevents.

Examples in Practice

Here are real-world vignettes that show these benefits in action:

Example 1: Commercial Underwriting Turnaround

A midsize carrier was struggling with long cycle times — 10 business days on average to underwrite standard commercial submissions. With AI-powered document extraction:

Exposures and key values were automatically parsed from submission packs.

Exceptions were flagged instantly for human review.

Result: Turnaround dropped to 24 hours for standard cases.

👉 Business Outcome: Improved broker satisfaction, higher bind rates, and a measurable reduction in lost opportunities due to slow response.

Example 2: Health Payer Prior Authorization

A health payer faced rising prior authorization backlogs due to manual review of medical records. By implementing an AI document management system:

Medical records were ingested and structured automatically.

Appeals fell as records were parsed with higher accuracy.

👉 Business Outcome: Faster patient care approvals, improved provider relationships, and reduced administrative expense ratios.

Example 3: P&C Renewal Compliance

A regional property & casualty firm had compliance gaps during renewals — missing disclosures triggered an audit escalation. With continuous compliance checks:

Every renewal was automatically validated against regulatory requirements.

Missing clauses triggered alerts before policies went out.

Result: Renewal errors were eliminated and audit escalation risk disappeared.

👉 Business Outcome: Lower regulatory risk, higher confidence from reinsurers, and strengthened governance posture.

✅ Together, these benefits and examples answer the C-level question: “How will AI affect the insurance industry?” — not with vague promises, but with measurable outcomes across cycle time, accuracy, cost efficiency, customer retention, and regulatory risk.

Hours with structured risk summaries for ai underwriting

Claims

Backlogs; missing attachments

Automated intake, triage, and SIU flags

Compliance

Spot checks and manual audits

Continuous checks and audit-ready evidence

Customer experience

Slow responses, manual calls

Quicker settlements and proactive communications

BCG’s field data shows ~50% faster claims and ~20% cost reductions when these flows are automated; McKinsey’s 2025 report frames AI as a lever to reinvent the end-to-end value chain.

Role of AI in Healthcare

How to Implement: A Practical Blueprint for Insurance Document AI

1. Map Value Pools

Begin by identifying where document friction is costing the most time or money. Common hotspots include:

FNOL (First Notice of Loss) submissions delayed by messy PDFs.

New-business submissions requiring hours of manual keying.

Claims packets that take days to review. This step ensures you’re not experimenting blindly — you’re targeting the highest-impact processes first.

2. Assemble a Unified Ingestion Pipeline

Rather than building multiple silos, set up a single ingestion and normalization layer that every team can use.

Standardize handling of PDFs, scanned images, broker emails, and medical records.

Ensure metadata tagging and classification at the point of entry. This gives the business one source of truth and prevents duplicate efforts across underwriting, claims, and servicing.

3. Train on In-House Documents

Generic models won’t cut it in insurance. Accuracy comes from feeding your own document corpus:

Labeled sets of broker submissions, policy forms, claims packets, and medical files.

Training entity extraction (e.g., policyholder names, loss dates) and classification models tuned to your business.

This makes outputs usable from day one — not theoretical.

4. Start Small, Measure Fast

Avoid “big bang” rollouts. Instead:

Launch with one line of business or one document type.

Track clear metrics: cycle-time reduction, accuracy of extracted fields, leakage reduction, and user satisfaction. Within weeks, you’ll know if the ROI is real — and you’ll have data to convince skeptics.

5. Human-in-the-Loop Workflow

AI doesn’t replace staff; it augments them.

Route low-confidence predictions to adjusters or underwriters.

Capture corrections automatically, feeding them back into model retraining. This creates a self-improving loop, where accuracy increases with use.

6. Governance & Audit Readiness

Insurance is a regulated industry — controls can’t be an afterthought.

Build in logging, access controls, and explainability from the start.

Provide audit trails showing why the AI extracted a specific field or flagged a risk. This makes regulatory reviews smoother and reduces compliance risk.

7. Scale Across Lines and Functions

Once proven in one workflow, expand gradually:

Extend ingestion across multiple lines (auto, health, property, specialty).

Integrate with policy admin systems, claims platforms, and CRM tools.

Layer in advanced decision-support — e.g., AI-driven underwriting risk scores or claims triage prioritization. This step transforms AI from a pilot project into an enterprise-wide capability.

✅ Final Takeaway: This blueprint transforms AI adoption from a buzzword into a structured operating model. By following it step by step, insurers move from pilots to enterprise-wide transformation — achieving measurable improvements in speed, accuracy, cost, compliance, and customer satisfaction.

How Alltius Helps: Turning Document Chaos into Operational Intelligence

At Alltius, we’ve built a reusable document intelligence layerpurpose-built for insurance. Unlike generic automation tools or one-off OCR scripts, our system plugs directly into your existing technology stack and starts delivering value without the need for core system replacement.

Here’s how it works in practice:

Universal ingestion Alltius can process virtually any insurance document — policy forms, medical records, loss runs, ACORD applications, adjuster notes, even handwritten or scanned submissions. Structured, semi-structured, or fully unstructured — our ingestion layer normalizes them into machine-readable formats instantly.

Deep insurance-specific NLP extraction Instead of surface-level keyword spotting, Alltius applies advanced natural language processing (NLP) tuned for insurance language. It extracts exposures, coverage clauses, exclusions, conditions, and claimant details with context — not just text. This reduces missed details and transcription errors, giving underwriters and adjusters the complete picture at once.

Underwriting and claims mapping Extracted data isn’t just dumped into a spreadsheet. Alltius maps it to actual underwriting and claims workflows — rating factors, risk scoring, FNOL intake, compliance checklists. This means documents flow directly into decision-ready formats, cutting cycle times dramatically.

Built-in compliance guardrails Every document processed by Alltius is logged with a full audit trail, ensuring that regulatory requirements are met automatically. Whether it’s Solvency II in Europe, HIPAA in healthcare, or NAIC standards in the US, compliance isn’t an afterthought — it’s embedded into the process.

Connectors to core policy systems Alltius integrates with the systems insurers already use — Guidewire, Duck Creek, Sapiens, custom-built PAS, or claims platforms. No rip-and-replace needed. Our APIs and connectors ensure data flows seamlessly into existing environments, reducing disruption and accelerating ROI.

The result? Insurance companies don’t just “experiment with AI.” They see tangible outcomes fast — faster underwriting turnaround, reduced claims leakage, lower administrative costs, and stronger compliance posture — all without overhauling their core systems.

A system that ingests, stores, indexes, and—critically—extracts structured data from insurance documents so downstream systems can act on facts rather than PDFs.

By converting narratives, medical notes and broker submissions into structured risk attributes. Underwriters receive prioritized insights and can focus on judgment rather than data entry.

No. The right question is how will AI replace routine tasks within underwriting? Machines handle volume and consistency; humans keep judgment, negotiation and edge-case risk assessment.

Underwriting, claims, product and compliance teams remain owners; however, data scientists, model stewards, and document operations roles become central to running and improving the system.

Yes—modern OCR + domain-tuned models can extract structured fields from messy inputs; human review handles edge cases and improves models over time.

Absolutely. Start with one high-value use case, measure ROI, and scale. Smaller firms often realize faster payback because manual costs are proportionally higher.

Data quality, bias in models, and insufficient governance. Mitigate by human review, logging, and periodic model audits.

Pilot benefits often appear within weeks to a few months; enterprise-wide gains follow as models are reused across workflows.

Make life easier for your customers, agents & yourself with Alltius' all-in-one-agentic AI platform!