Build intelligent, secure and accurate GenAI assistants for your customers, support and sales teams

© 2025 Alltius Inc

Traditional lending relies heavily on manual, labour‑intensive processes. From paperwork and data entry to compliance and underwriting checks, manual loan origination inflates costs at every stage. In response, loan automation is emerging as the essential fix, especially via auto loan origination software, automated mortgage processing, and automated loan origination system platforms that streamline workflows, reduce error, improve turnaround times, and cut expenses.

What is loan origination? It’s the full process of moving from borrower application to final loan funding: intake, document collection, eligibility checks, underwriting decision, approval, pricing, and disbursement. Manual processes involve humans in nearly every step—opening envelopes, typing data, calling credit bureaus, manual compliance review. These repetitive manual tasks drive cost, introduce errors, and delay decisions.

A 2022 Accenture analysis emphasised that “highly manual and repetitive processes are some of the main contributors to loan origination costs.” They recommended lenders evaluate every stage for automation opportunities, for example to increase efficiency via robotics process automation to mimic human actions in routine tasks.

Here’s how auto loan origination software, loan origination automation, and automated loan origination system solutions tackle the inefficiencies:

Moreover, Accenture reports a lender that implemented a cloud‑based commercial lending origination system with automation tools accelerated approval time by 26 % and sped up disbursements under US $350,000 loans.

An auto loan origination platform automates borrower data ingestion, document extraction, credit bureau interfacing, underwriting, and pricing. This automated mortgage processing system drastically reduces manual data entry. According to a systems integrator case, customer information vetting and unstructured data integration automation led to “substantial cost reduction”.

Small business loan automation software can reduce per‑application processing expense by 30‑50 % as manual tasks like data entry, analyses of GST or invoice data, compliance are automated. Business borrowers benefit from faster turnaround and clarity.

BCG research suggests banks can already deploy automated decisioning for loans up to US$1 million. That means many small and mid‑size corporate loans can leverage loan origination automation instead of manual review.

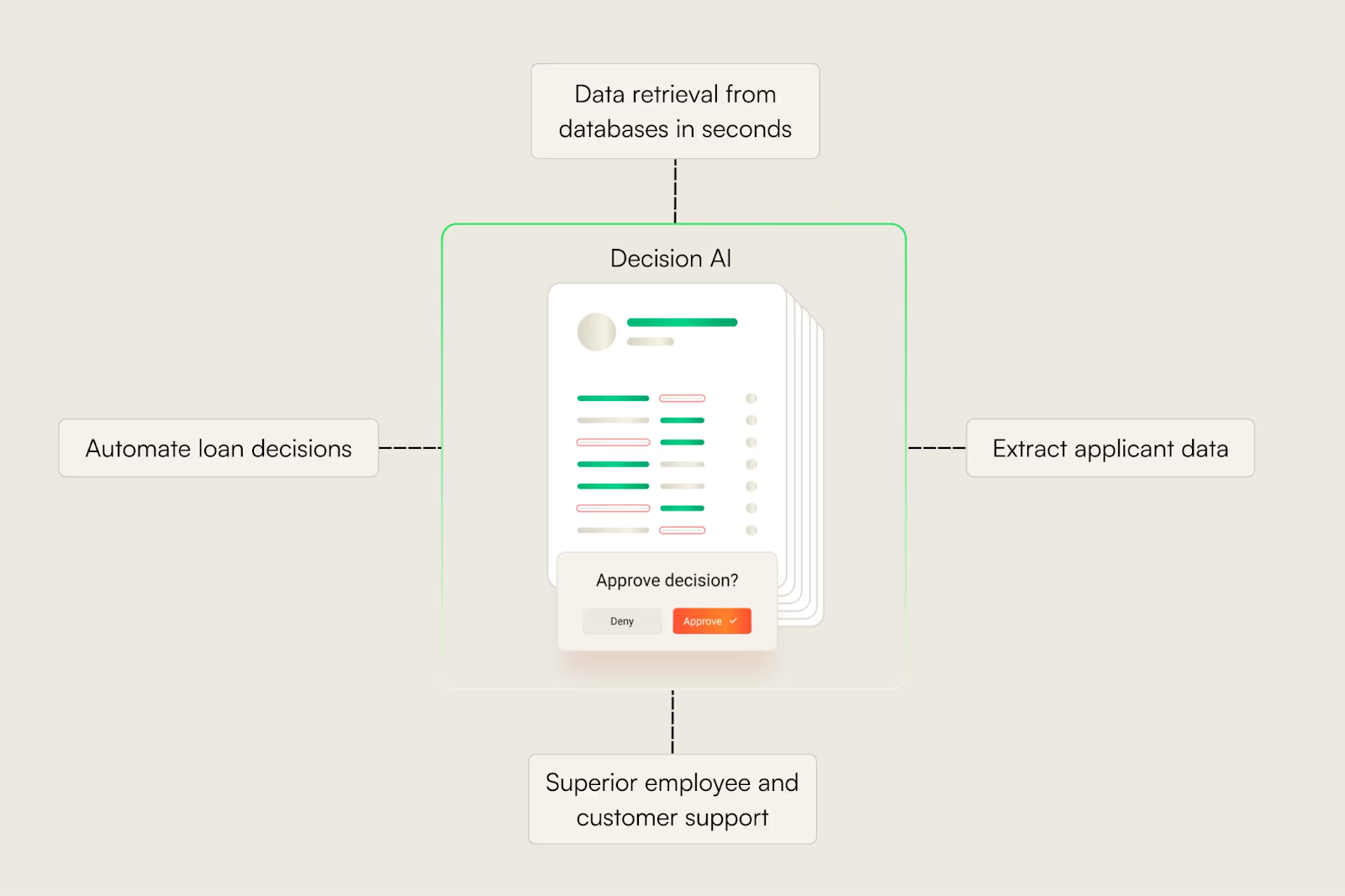

For years, only top-tier banks could afford advanced risk models and proprietary loan origination platforms. But Decision AI is changing that dynamic. Mid-market lenders—regional banks, NBFCs, and fintechs—can now implement loan origination automation with embedded decisioning logic that rivals enterprise systems in speed and sophistication.

Decision AI uses historical data, real-time signals, and underwriting rules to automate key approvals. When embedded within auto loan origination software, it enables mid-sized lenders to process more applications without hiring more analysts.

A Bain & Company study noted that “banks using automated decisioning models reduced underwriting cycle time by over 40% while expanding to underserved segments” (source). For mid-market lenders, this means faster loans, better margins, and stronger market presence—without inflating operating cost.

By pairing decision intelligence with automated mortgage processing or auto loan origination, smaller institutions gain strategic parity with larger players—and can differentiate on experience, not just pricing.

Manual loan origination not only costs more—it slows speed to borrower, hurts experience, and risks competitiveness. McKinsey highlights that improving operating leverage requires digitization of lending workflows; technology enables revenue growth without proportional cost growth.

BCG notes only about 25 % of financial institutions have effectively used automation to their competitive advantage—most still at experimental stages—meaning leaders stand to gain significant advantage via early adoption of automated loan origination systems.

Morgan Stanley analysis also predicts the share of tasks done by technology rising from 22 % to 34 % by 2030, shrinking purely human contributions and emphasising automation’s growing role in cost‑effective service delivery.

Beyond cost savings, automation supports financial inclusion and new business. BCG research shows inclusive lending powered by proper loan origination software enhances long‑term profitability—for example, narrowing wealth disparities could unlock tens of billions in annual revenue for lenders.

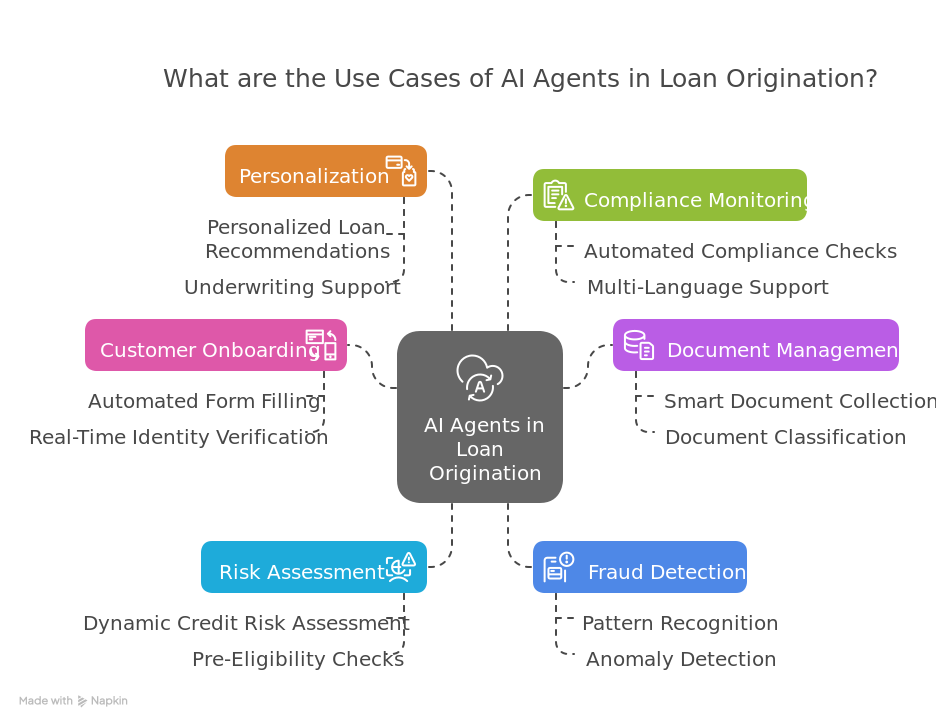

Alltius brings a modular approach to automating end-to-end loan origination by focusing on two critical infrastructure layers: Document Intelligence Pipelines and Decision Orchestration APIs. Unlike monolithic platforms that force lenders into rigid workflows, Alltius integrates with existing systems via lightweight APIs, accelerating adoption while minimizing technical debt.

Alltius ingests structured and unstructured borrower data—bank statements, GST returns, KYC documents, invoices—through its document intelligence pipeline. The system applies a multi-pass architecture using OCR, semantic parsing, and embedded contextual models to extract high-accuracy entities and flag anomalies.

Sitting on top of lender-defined policies, Alltius enables risk automation via a serverless decision orchestration engine. This orchestration abstracts complex decision paths into modular, testable decision nodes.

Alltius is not a monolith—it is built to embed. The platform integrates with leading auto loan origination software, automated mortgage processing systems, and custom CRMs. This makes it ideal for mid-market NBFCs or digital lenders that need automation without replatforming.

🔧 Example: A regional NBFC using Alltius processed over 65% of SME loan applications (sub ₹10L) through straight-through processing after six weeks of implementation—cutting analyst review time by 43%.

Loan origination isn't just about approvals—it's about speed, precision, and scale. Alltius delivers all three by combining deep document understanding with flexible, API-first decisioning.

Whether you're a digital-first lender scaling fast or a traditional NBFC modernizing legacy systems, Alltius helps you get to “yes” faster—with fewer errors, fewer handoffs, and full control over every rule and risk path.

🚀 Faster originations. Lower costs. Happier borrowers.

Let’s build the next-gen lending stack—without ripping out the old one.

👉 Book a demo to see Alltius in action.

Manual loan origination systems are not just inefficient—they're structurally unfit for modern lending volumes and expectations. As borrower data grows more unstructured and compliance demands evolve, legacy workflows break down. That's why scalable solutions like loan automation, auto loan origination software, and automated loan origination systems are fast becoming non-negotiable.

Studies from McKinsey, Accenture, and Bain reveal:

Alltius brings these benefits to reality—without forcing lenders to rip out their existing LOS or CRM. Our platform automates intake, evaluation, and triage with intelligent agents that adapt to policies, borrowers, and document types in real time.

Want to reduce turnaround time and scale smarter?

👉 Book a walkthrough with Alltius or start a free trial to see how automated loan origination can transform your operations.

Make life easier for your customers, agents & yourself with Alltius' all-in-one-agentic AI platform!

See how it works >>

Book a 30-minute demo & explore how our agentic AI can automate your workflows and boost profitability.